Recently the question was posed to me: should a small business (5 people) offer insurance to their staff? The person asking had an independent plan but wanted a greater peace of mind from employer sponsored health insurance. This person was 30 years old.

Yes, the business should offer it, but don’t expect great things.

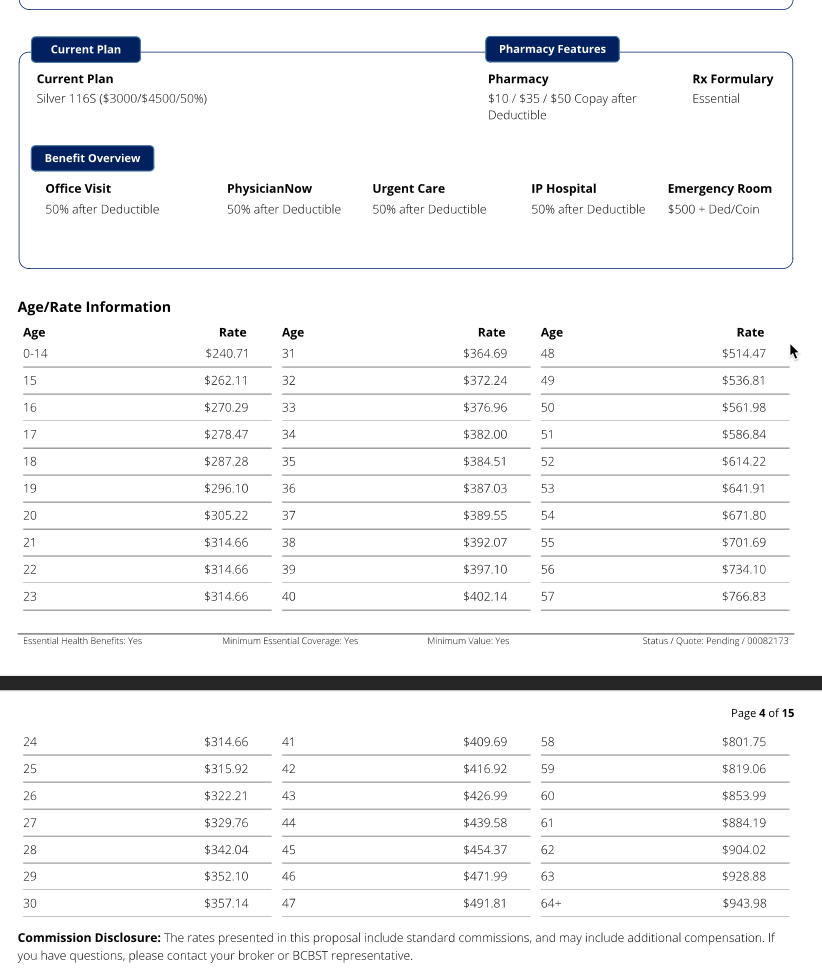

I’m in Tennessee, attached is my rate schedule. As long as two employees have coverage, we are a group. Owners count towards those two people.

A 30yo is free, $12/day.

The catch is that it is a high deductible plan (HDP) so out-of-pocket costs will be $4500/person if you max out benefits, or $9000/family.

If you compare plans on HealthCare.gov I think you’ll find the rates are comparable, but you can get worse-but-cheaper plans. The real upside here is risk reduction and tax benefits if you have an HSA compatible plan and you itemize, maybe $1600 in tax savings*.

Your overall risk profile isn’t likely to change much as long as you have some level of benefits — but check the details**. The ACA mandates minimum coverage for ALL plans, meaning the total-out-pocket costs (premiums + medical expenses) are within a set range.

Vision and dental, for whatever reason, are typically inexpensive.

Bottom line:

1. Insurance is a raw deal no matter what.

2. You may or may not be better of with an independent plan vs a group plan

3. IMHO, there isn’t a good reason for your employer not to offer a plan unless the costs are significantly higher where you live. And I say this AS a business owner with 6 employees and 2 owners.

*If you max out the family contribution limit of $8300, your potential tax savings are $8300 * [Tax Bracket]. You can also invest extra money in your HSA, allowing you to grow the money tax free for healthcare expenses.

**Prescriptions, specialties, coverage for your preferred doctor/hospital, possible travel for covered specialists depending on your location. Absolutely know what hospitals are covered no matter what, the “wrong” hospital can cost you thousands and thousands compared to the “right” hospital across the street.

0 Comments